We made a review of simple strategies for a client that is developing a portfolio management system for trading cryptocurrencies. The idea was to provide the client with simple but realistic strategies to illustrate the interest of its software.

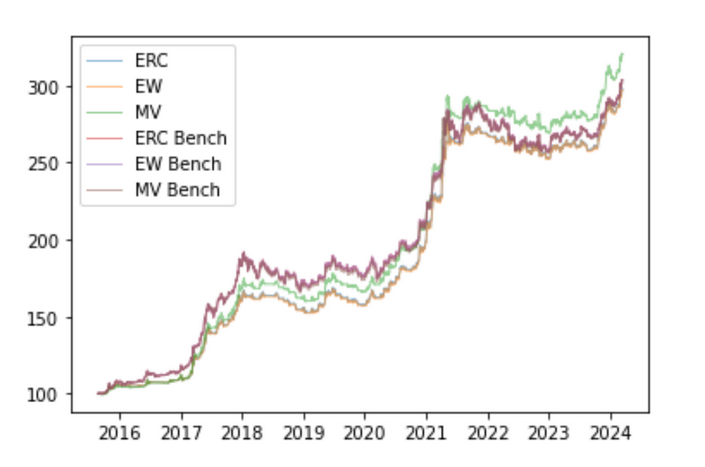

We implemented a simple momentum strategy. Momentum strategies are classic and applied in different asset classes. The strategy is simulated between February 2015 and March 2024 on a universe of 8 main cryptocurrencies with an rate of 10% (including BTC and ETH). Different values for the momentum interval were tested, 15 days gives the best results. To be robust to the date of initialization of the performance calculation, we calculate 15 signals in shifting the calculation origin by one day. Each portfolio is rebalanced every 15 days, the cryptos are equally weighted. By curiosity, we build benchmarks containing all crypto on the same model equally weighted in order to evaluate the interest of this simple strategy. Then we aggregate these 15 series into an equally weighted portfolio or weighted by weights based on risks (MV, ERC). We construct aggregated benchmarks on the same model.

The aggregated versions have a sharpe ratio higher than the benchmarks. The Min Var version is the most efficient and display a sharpe ratio of 1.5 on the full period of simulation. Benchmark displays a sharpe ratio of 1.31.

Acuity Analytics

At Acuity Analytics, we understand that every data-informed decision process development is an exploration rather than a dogmatic assertion.

Join us in our pragmatic approach to data analysis, where we humbly aspire to make meaningful contributions to your applications.

Contact

contact@acuity-analytics.eu

Acuity Analytics

SASU au capital de 1000 euros 987 753 142 R.C.S Paris